Automatic bill and meter data capture

Connect directly to your energy accounts so every bill and every meter automatically uploads to the platform.

Connect directly to your energy accounts so every bill and every meter automatically uploads to the platform.

Termina's software platform is free to use when combined with procurement so you can choose a subscription or save money while using us.

Instant customisable exports so data can be uploaded anywhere.

Termina's platform is totally free to use with our saving split model. Start for free today.

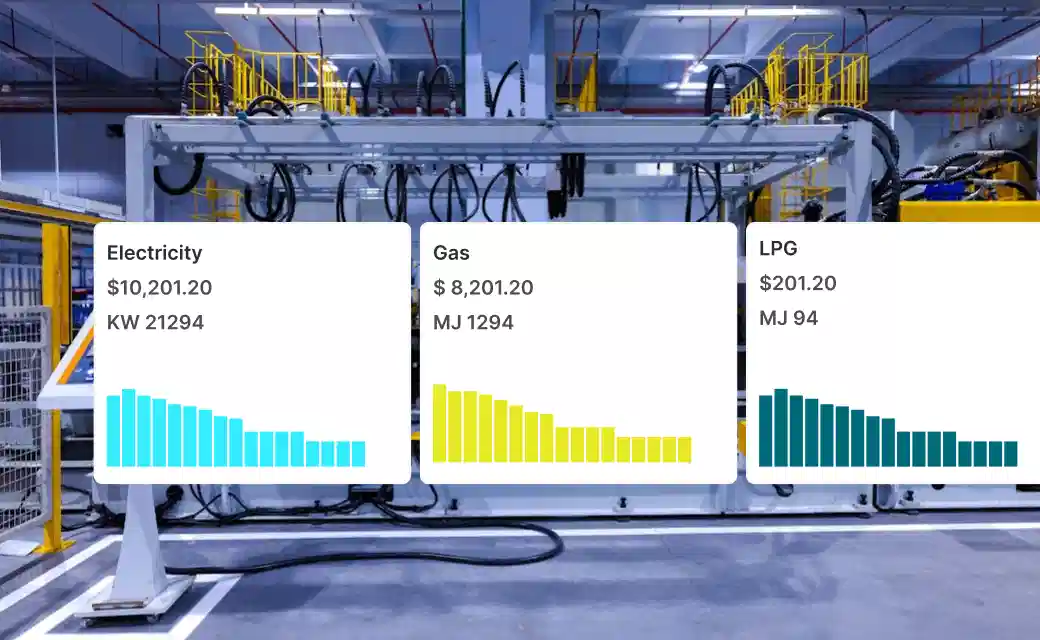

Gas, electricity, embedded network,and LPG accounts from every marketin one place automatically.

Collect data in seconds, not weeks.

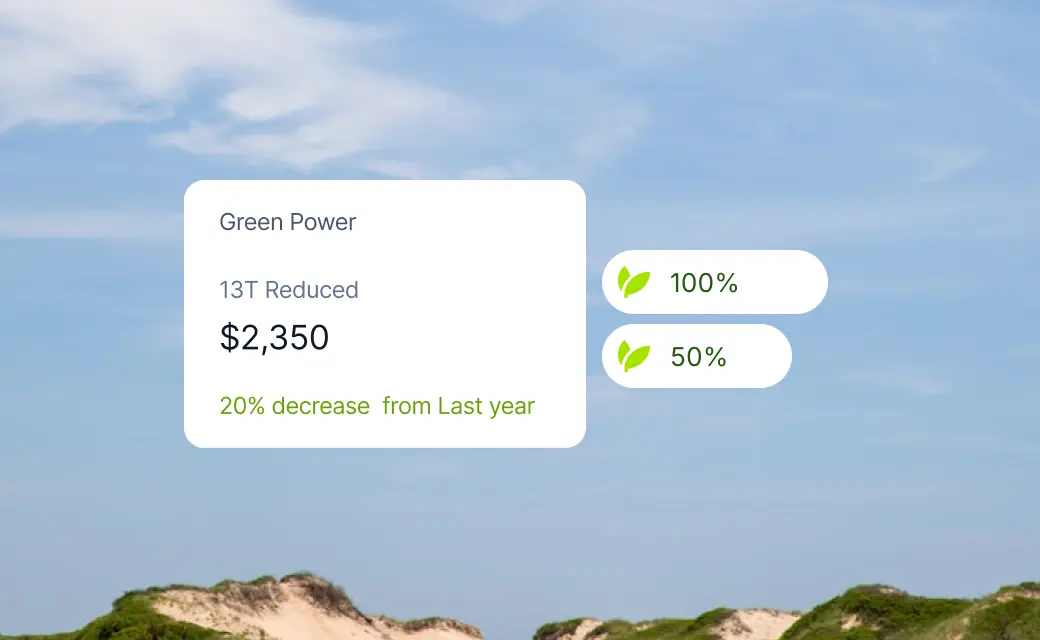

Optimise Greenpower so you can reduce energy costs while increasing investment in Greenpower.

Export kWh and MJ data for every energy account so you don’t have to upload each energy bill manually.

You already need your data structured. Start for free today.

AASB S2 Climate-related Disclosures is Australia's mandatory standard for climate-related financial reporting. It requires certain entities to disclose information about climate-related risks and opportunities across four pillars: governance, strategy (including scenario analysis), risk management, and metrics and targets - including Scope 1, 2, and eventually Scope 3 greenhouse gas emissions.

The TCFD was a voluntary framework with recommended disclosures. AASB S2 supersedes it in Australia - using the same four-pillar structure but with mandatory legal force, more granular requirements, prescribed climate scenarios (1.5°C and well exceeds 2°C), mandatory external assurance, and penalties up to $15 million or 10% of annual turnover for misleading statements.

AASB S2 is closely aligned with IFRS S2, with some Australian-specific modifications: it prescribes specific climate scenarios, does not currently require industry-based metrics, and includes Australian transition provisions and assurance phasing. If your parent reports under IFRS S2 globally, this does not exempt you from a separate AASB S2 report if you meet Australian thresholds.

You must report if your entity prepares a financial report under Chapter 2M of the Corporations Act and meets at least two of three size criteria for any group.

Group 1:

≥$500M revenue, ≥$1B assets, or >500 employees.

Group 2:

≥$200M revenue, ≥$500M assets, or ≥100 employees.

Group 3:

≥$50M revenue, ≥$25M assets, or ≥100 employees.

NGER reporters and qualifying asset owners (≥$5B AUM) are also captured.

Group 1: financial years beginning on or after 1 January 2025.

Group 2: from 1 July 2026.

Group 3: from 1 July 2027.

The reporting period aligns with your financial year. For a July–June entity in Group 1, the first period is FY26 (1 July 2025 – 30 June 2026), with the sustainability report due within three months of year-end.

Yes. AASB S2 applies to any entity with Chapter 2M reporting obligations that meets the size thresholds - listed or unlisted, public or proprietary. Many of the first Group 1 reports published in early 2026 are from private unlisted entities.

Scope 1 (direct emissions from sources you own or control) and Scope 2 (indirect emissions from purchased electricity, measured location-based). Market-based Scope 2 is also required but has transitional relief for the first three years. Scope 3 emissions have a one-year grace period and become mandatory from your second reporting period.

Multiply electricity consumed at each site (kWh) by the location-based emission factor for the relevant state grid, published annually in the National Greenhouse Accounts Factors workbook. For multi-site portfolios, the challenge is consolidating data across many NMIs, reconciling billing periods to your financial year-end, and separating grid imports from on-site solar generation. Energy data platforms like Termina can automate this and provide the audit trail that assurance demands.

Solar self-consumption reduces your grid imports and therefore your Scope 2 emissions - you report net grid consumption multiplied by the relevant emission factor. Exported solar is not counted in your Scope 2. For batteries, emissions depend on the charging source: grid-charged electricity carries the grid emission factor; solar-charged carries effectively zero. Accurate interval data that distinguishes between grid, solar, and battery flows is essential. Termina reports this in a few clicks.